Case Study

Smart energy management for buildings

Identifying product/service growth opportunities in energy management for commercial, office, and residential buildings

Identifying product/service growth opportunities in energy management for commercial, office, and residential buildings

CamIn works with early adopters to identify new opportunities enabled by emerging technology.

of CamIn’s project team comprised of leading industry and technology experts

Our energy utilities client wanted to confirm energy management products & services to decarbonise their customers’ building assets. CamIn went through its proprietary process to confirm 5 quick-win products and services that unlock instant value to new customers within 6 months.

Product & service innovation

After new regulations were introduced in our client's operating regions in Europe, their customers were looking for solutions to decarbonise their building assets quickly within the next 6 months. Retrofit demand surged 28% especially in the Nordics, highlighting urgent need for effective solutions. The client had developed a concept of product areas, however needed a shortlist of confirmed products and services that were technologically feasible, desired by their customers, and easily implementable. The client lacked the confidence to conduct the necessary analysis within the required breadth, depth, and timeframe. They required CamIn to support them in identifying the correct products for a quick development and launch.

4 |

Determined 4 key application areas for commercial, office, and residential building energy management: Monitoring, Demand response, Grid interactivity, Optimisation. |

20 |

Identified and analysed 20 technology use cases in terms of their likelihood of commercialisation, their time to commercialisation, and the scale of their likely impact on the market. |

9 |

Isolated the 9 most promising use cases, principally based on grid interactivity for commercial buildings, based on their high likelihood of commercialisation and their high market impact. |

9 |

Combined the 9 highest-scoring use cases into 5 strategically important product/service areas, in which CamIn will develop business cases for investment. |

By combining the 9 highest-scoring use cases, CamIn identified 5 strategically important product/service areas for the client.

The client is piloting all 5 products with credible strategic partners and have successfully satisfied current customer demand.

CamIn derisked the client's $10 million investment into now product opportunities, opening new lucrative revenue streams.

Download our detailed case study to learn more about how CamIn and our hand-selected expert project team delivered these results for our client.

.svg)

Smart energy management solutions enable buildings to monitor, control, and optimise their energy usage in real time. These systems integrate technologies such as sensors, IoT devices, AI-driven analytics, and demand response platforms to improve energy efficiency, reduce carbon emissions, and lower operating costs. In practice, this may include intelligent HVAC control, real-time energy consumption dashboards, predictive maintenance, and grid-interactive capabilities. For utilities, such solutions unlock opportunities to offer value-added services to commercial, office, and residential customers.

Smart energy management is becoming essential for utilities seeking to remain competitive, compliant, and customer-focused in a rapidly evolving energy landscape.

Over the next decade, smart energy management will fundamentally transform the utilities industry. It will shift the core business model from simply supplying electricity to delivering intelligent, data-driven energy services. This evolution will impact grid operations, customer engagement, regulatory alignment, and long-term competitiveness.

Key impacts over the next 10 years will include:

Strategic shift for utilities:

Utilities will evolve into hybrid data-energy providers. Those that invest early in smart energy management will gain:

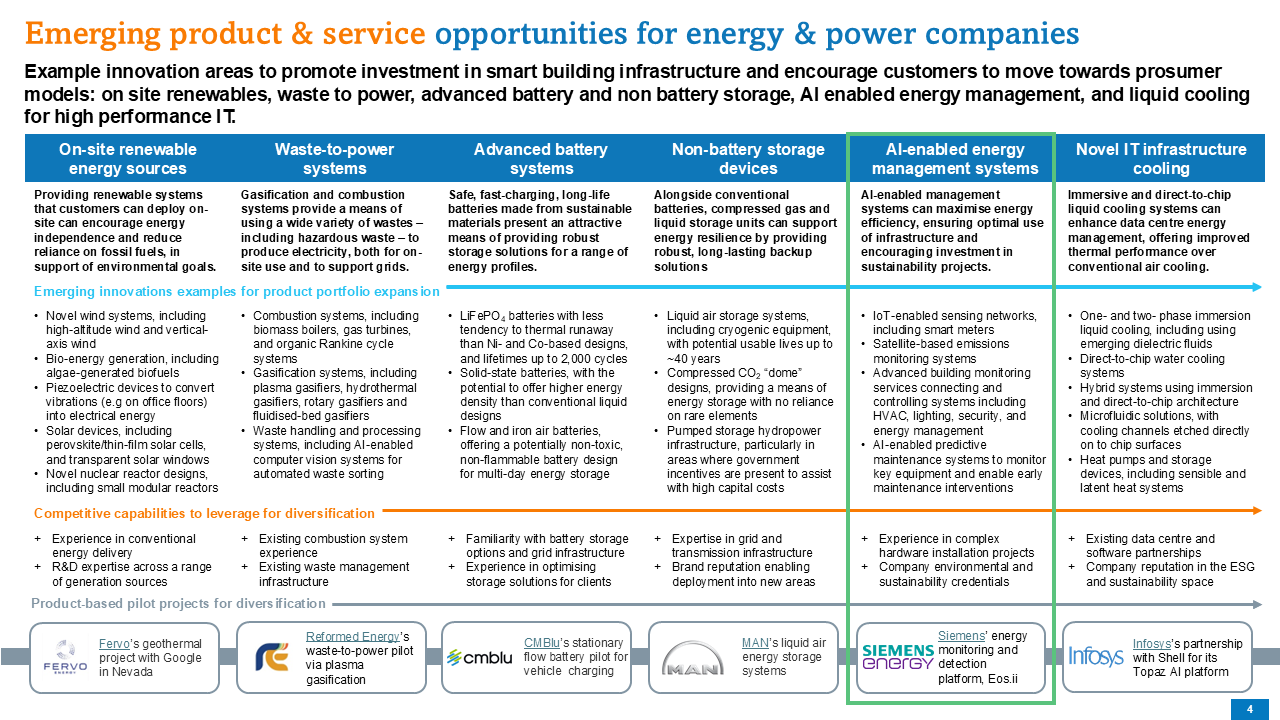

The landscape of smart energy management is being reshaped by a convergence of digital, connectivity, and control technologies, enabling new levels of visibility, automation, and responsiveness in building energy systems. These emerging technologies support utilities and building operators in achieving ambitious decarbonisation, cost-efficiency, and resiliency goals. The most impactful innovations fall into the following subsegments:

AI and Advanced Analytics

IoT and Sensor Networks

Digital Twins and Simulation Technologies

Connectivity and Edge/Cloud Integration

Demand Response and Grid-Interactive Technologies

Cybersecurity and Resilient Infrastructure

Smart energy management in buildings is being driven by tightening climate regulations, grid flexibility needs, rising energy costs, digital innovation, and growing ESG, financial, and consumer pressures.

Smart energy management in buildings leverages AI, IoT, digital twins, and advanced controls to optimise energy use, integrate renewables, enable flexibility, and unlock new value streams across grids and districts.

Adoption of AI-driven optimisation for local renewables and storage faces mainly medium-level barriers around cost, integration, regulation, and scalability, giving an overall feasibility score of medium-high.

| Difficulty | Barriers to Adoption |

|---|---|

| High | Installing sensors, controllers, and optimisation software across diverse building portfolios requires significant CapEx, slowing ROI justification. |

| Medium | Older HVAC, storage, and BMS systems may lack interoperability with AI platforms, requiring costly hardware upgrades or middleware. |

| Medium | Participation in flexibility and VPP markets depends on evolving regulatory frameworks, limiting near-term revenue certainty for building owners. |

| Medium | AI optimisation relies on high-quality data from multiple assets (PV, batteries, HVAC, etc.) Lack of standardised data formats complicates integration. |

| Medium | Connecting building systems to cloud/AI optimisation raises risks of cyberattacks or data breaches, requiring robust protections. |

| Medium | AI optimisation that shifts loads (e.g., HVAC) must balance energy savings with tenant comfort, otherwise risking user resistance. |

| Medium | Savings from AI optimisation may depend on volatile energy prices and utility tariffs, limiting confidence in long-term ROI. |

| Medium | Numerous EMS and VPP providers exist, with different proprietary platforms. Buyers risk lock-in and lack of long-term support. |

| Medium | To deliver grid services, systems must meet strict communication and control standards (e.g. OpenADR), adding compliance burdens. |

| Medium | Optimisation strategies may perform well in pilots but face complexity when scaled across hundreds of diverse buildings with varying infrastructure. |

Buildings, campuses, and districts face regulatory, financial, and social pressure to optimise renewable integration and energy efficiency, creating strong demand for AI-enabled optimisation systems.

Globally, the building energy management systems (BEMS) market was valued at $7.1 bn in 2024 and is projected to grow to $20.4 bn by 2033, driven by the need to integrate renewables and storage. The distributed energy resource management systems (DERMS) market, closely aligned with AI-based optimisation, was valued at $0.6 bn in 2024 and is expected to grow to $1.4 bn by 2029.

Europe’s Energy Performance of Buildings Directive (EPBD) revisions mandate smart technologies to reduce energy consumption in all new and renovated buildings by 2030. In the US, the DOE projects a significant growth in commercial buildings adopting grid-interactive efficient technologies by 2030, enabled by AI and automation.

If even 10% of EU’s 220 million buildings adopt AI-driven optimisation at €20-50k per building (one-time system, and ongoing SaaS), the addressable market could reach €40-100 bn, with significant upside in North America and Asia.

In short: AI-driven energy optimisation is technically ready, with rapid scaling likely in 1–3 years as regulation and business models align.

| Factor | Assessment | Overall outlook |

|---|---|---|

| Political | EU EPBD, U.S. IRA, and Asian smart building policies drive adoption of AI-enabled energy optimisation. | Positive |

| Economic | Rising energy prices and volatility incentivise demand-side optimisation; grid services create new revenue streams. | Positive |

| Social | Tenants and corporates increasingly demand low-energy, green-certified buildings; AI optimisation enhances ESG credentials. | Positive |

| Technological | IoT, AI, and digital twins are mature and cost-effective; integration with DERMS and VPPs is technically proven. | Positive |

| Legal | Stricter efficiency codes (EPBD, U.S. state standards) mandate digital optimisation and data reporting for compliance. | Positive |

| Environmental | Net-zero targets require cuts in emissions; optimisation maximises self-consumption and reduces carbon intensity. | Positive |

Utilities are well positioned in terms of regulatory access, customer base, and infrastructure, but must strengthen AI/ML, SaaS scaling, and device-level integration through partnerships or acquisitions.

Utilities bring strong regulatory, infrastructure, and customer-side expertise, giving them a strong position to adopt AI-enabled optimisation. However, they may lack advanced AI/ML development and SaaS platform capabilities, requiring partnerships with specialised vendors and developers (e.g. Stem, BrainBox AI, AutoGrid) to fill technology and scaling gaps.

| Capability | Rationale | Current fit estimate | Current fit summary |

|---|---|---|---|

| Grid and energy operations knowledge | Deep expertise in managing generation, load balancing, and grid integration. | Strong | Utilities already operate distributed energy and flexibility programs; strong “market access” to customers and regulators. |

| Regulatory & compliance expertise | Navigating energy market rules, tariffs, demand-response programs. | Strong | Active role in regulatory processes and compliance-heavy markets; able to ensure alignment with grid codes and flexibility services. |

| Customer & industry partnerships | Partnerships with building owners, municipalities, and corporates. | Strong | Utilities already serve C&I and residential customers; strong channels for adoption of optimisation platforms. |

| Cybersecurity & data governance | Ensuring resilience, compliance, and customer trust in connected energy systems. | Strong | Utilities already invest heavily in cybersecurity for critical infrastructure; good baseline but must extend to customer systems. |

| Energy hardware integration (batteries, PV, EV chargers) | Ability to integrate and manage diverse DER assets. | Strong | Existing pilots and partnerships in storage, EV charging, and renewable integration provide a solid foundation. |

| Data infrastructure & analytics platforms | Handling metering, billing, and energy use datasets. | Moderate | Utilities manage large energy data streams but often lack advanced real-time AI analytics capabilities. |

| AI/ML optimisation expertise | Development of predictive optimisation algorithms for DERs. | Moderate | Some in-house pilots, but limited compared to specialised AI energy startups (e.g. BrainBox AI, AutoGrid) |

| Edge computing & IoT integration | Processing and controlling devices (batteries, EVs, HVAC) at scale. | Moderate | Utilities test IoT pilots (smart meters, demand response) but need stronger device-level control capabilities. |

| Commercial scaling & service models | Offering subscription-based optimisation or SaaS services. | Moderate | Utilities have experience with retail services but limited SaaS platform scaling expertise; may need new business models. |

| Industrial digitisation experience | Deploying IoT, digital twins, and monitoring in real environments. | Moderate | Strong in metering and asset monitoring; emerging capabilities in digital twin applications for buildings and grids. |

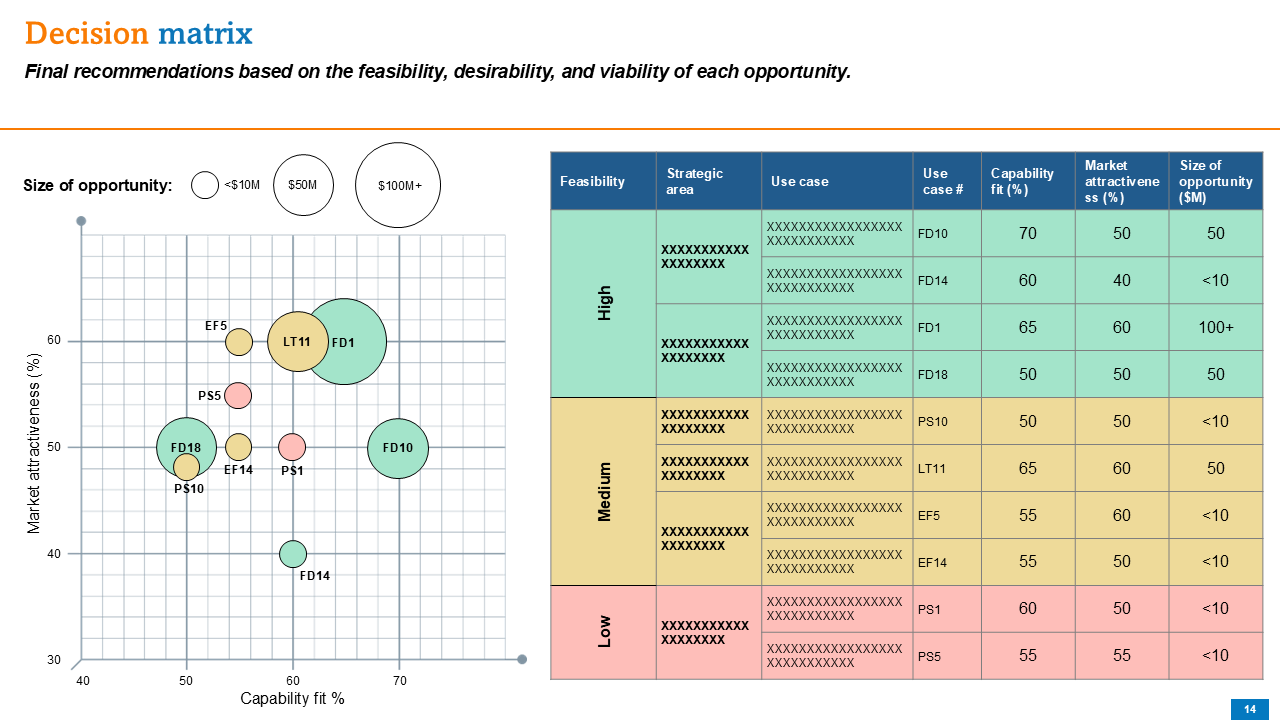

CamIn has identified and analysed 20 technology use cases in terms of their likelihood of commercialisation, their time to commercialisation, and the scale of their likely impact on the market. Then we isolated the 9 most promising use cases, principally based on grid interactivity for commercial buildings, based on their high likelihood of commercialisation and their high market impact. Finally, we have combined the 9 highest-scoring use cases into 5 strategically important product/service areas, in which CamIn will develop business cases for investment.