Case Study

Cognitive computing for financial services

Unlocked 6 new M&A offerings and upgraded 15 deal stages using AI and computing technologies

Unlocked 6 new M&A offerings and upgraded 15 deal stages using AI and computing technologies

CamIn works with early adopters to identify new opportunities enabled by emerging technology.

of CamIn’s project team comprised of leading industry and technology experts

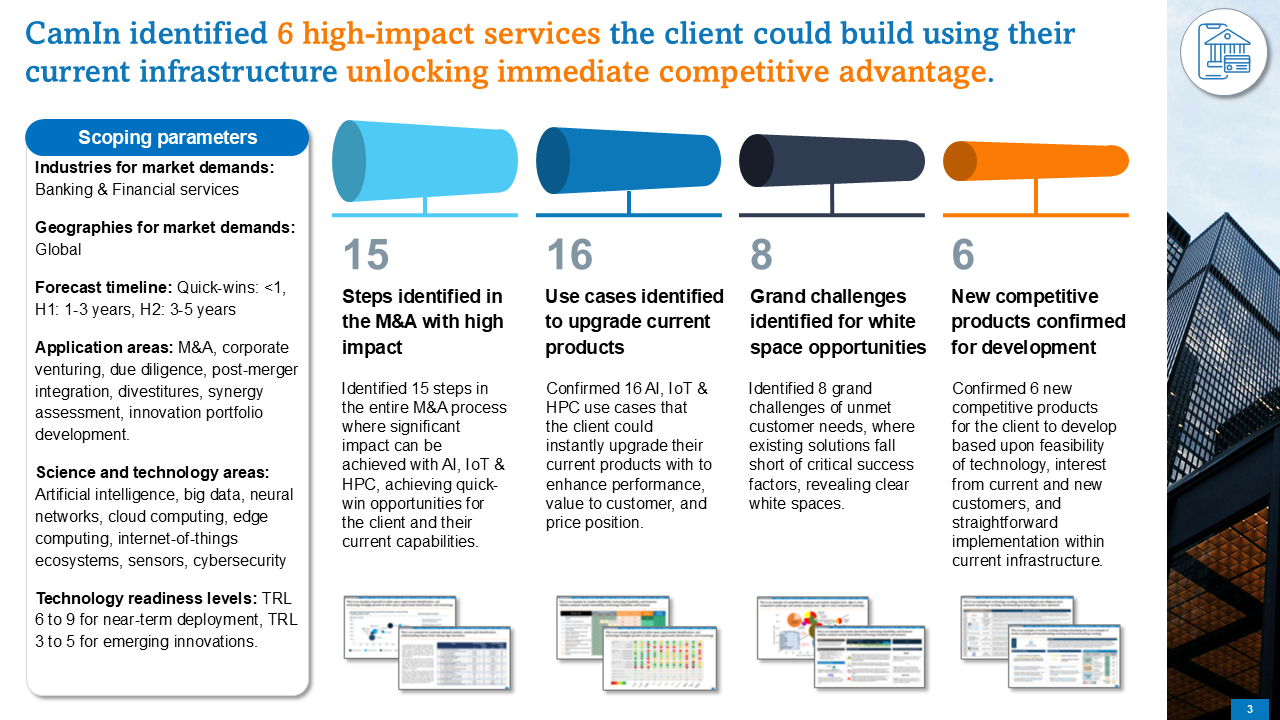

Our financial services client wanted to confirm how AI, HPC, and IoT upgrades their current services and unlocks new opportunities within 5 years. CamIn identified 6 high-impact AI services the client could build using their current infrastructure.

Product & service innovation

The client was losing ground in its multi-billion dollar M&A business as competitors gained an edge using AI to drive pricing advantages. Global M&A deal volumes have exceeded $4 trillion annually in recent years, with firms leveraging advanced analytics and automation achieving up to 20 percent faster deal cycles and significantly lower due diligence costs.

To stay competitive, the client needed to modernise its product and service offerings using AI, high-performance computing, Internet of Things technologies, and other digital innovations that could provide a first mover advantage over the next five years. The objective was to identify technologies that could improve deal execution, reduce risk, and capture greater market share in an increasingly data-driven M&A environment. Identifying the right approach required expertise in frontier technologies and strategic transactions that went beyond the client’s in-house capabilities.

%20.jpg)

15 | Identified 15 steps in the entire M&A process where significant impact can be achieved with AI, HPC, and IoT achieving quick-win opportunities for the client and their current capabilities. |

16 | Confirmed 16 AI, HPC, and IoT use cases that the client could instantly upgrade their current products with to enhance performance, value to customer, and price position. |

8 | Identified 8 grand challenges of unmet customer needs, where existing solutions fall short of critical success factors, revealing clear white spaces. |

6 | Confirmed 6 new competitive products for the client to develop based upon feasibility of technology, interest from current and new customers, and straightforward implementation within current infrastructure. |

6 new products confirmed for development based on tech feasibility, customer interest, and ease of implementation.

The client developed and piloted 4 out of the 6 products: 3 to capture quick-win opportunities and 1 to capture a white space.

The client confirmed the success of the product launches, generating revenue and de-risking their $10 million investment.

Download our detailed case study to learn more about how CamIn and our hand-selected expert project team delivered these results for our client.

.svg)

AI (Artificial Intelligence) and HPC (High-Performance Computing) enable financial advisory firms to automate, accelerate, and enhance key deal-making functions such as financial modelling, target screening, risk analysis, and due diligence. AI can ingest and analyse vast amounts of structured and unstructured data, including filings, financial reports, news feeds, and transaction histories, to uncover patterns and insights at a scale beyond human capability. HPC systems provide the processing power required to run these complex models in real time, enabling simulations, forecasts, and valuations that are both faster and more precise. Together, they create a next-generation advisory stack that transforms traditional workflows into intelligent, data-driven processes.

As deal volumes grow and competitive pressure intensifies, financial advisory firms are being pushed to deliver faster, smarter, and more precise insights. The sector is characterised by high data complexity, tight timelines, and increasing demands for strategic clarity. In this environment, Artificial Intelligence and High Performance Computing are becoming essential tools for gaining a competitive edge. Firms that adopt these technologies can streamline processes, enhance accuracy, and deliver more value to clients across the deal lifecycle.

AI, HPC, and IoT will transform the financial advisory landscape into a real-time, insight-led service model. Over the next decade, they will:

Several transformative technologies and platforms are coming into use and will expand significantly over the next decade:

A leading North American advisory firm implemented a proprietary diligence engine using AWS Textract, transformer-based NLP, and vector search. This reduced document review time by 60 percent and shifted analyst focus toward modelling and strategy.

Over the next 10 years, these tools will continue to evolve, powered by advances in quantum computing, federated learning for deal data sharing, and vertical AI agents for specific advisory use cases. This will allow firms to launch new service lines and operational models that are both more intelligent and more scalable.

Financial institutions are accelerating deployment of Edge and IoT solutions to achieve real-time security, resilient operations, smarter physical networks, and data-driven efficiency in an increasingly digitised, regulated, and competitive banking landscape.

Edge computing is rapidly approaching full commercial maturity, but large-scale banking adoption will hinge on resolving integration, security, and standardisation barriers, unlocking a step-change in real-time, resilient, and intelligence-driven financial infrastructure.

Edge computing is rapidly approaching full commercial maturity, but large-scale banking adoption will hinge on resolving integration, security, and standardisation barriers, unlocking a step-change in real-time, resilient, and intelligence-driven financial infrastructure.

Edge computing technologies, comprising distributed compute nodes, lightweight containerisation, MEC (Multi-access Edge Computing) architectures, and secure IoT device management, are now late-stage commercial (TRL 8–9) across telecoms, industrial automation, and increasingly financial services.

Production deployments are widespread in 5G networks, smart-manufacturing systems, and critical infrastructure, but financial-grade implementations still encounter commercialisation barriers: (i) integration complexity with legacy banking stacks; (ii) immaturity of unified orchestration tools capable of managing thousands of distributed nodes; (iii) stringent regulatory constraints on data residency, auditability, and operational resilience; and (iv) fragmented vendor ecosystems requiring alignment between telcos, cloud providers, and bank cybersecurity frameworks.

Given current deployment velocity, 1-3 years is a reasonable projection for broad adoption of discrete use cases (e.g. edge fraud scoring, smart ATMs, biometric verification), while 3-7 years is likely for fully integrated, enterprise-wide edge platforms underpinning real-time analytics, identity, payments, and smart-asset finance.

| Signpost | Comment | Likelihood |

|---|---|---|

| Large-scale reference deployments in regulated sectors | Multi-site, cross-jurisdictional edge deployments demonstrating resilience, fraud-reduction impact, and opex savings would materially de-risk adoption for major banks. | High |

| Convergence of MEC, 3GPP, and cloud-edge standards | Standards alignment will reduce vendor fragmentation and enable portable workloads across telco, cloud, and on-premise edge domains. | High |

| Decline in per-node hardware and connectivity costs | Falling prices for ruggedised edge nodes, secure enclaves, and 5G connectivity will make dense edge topologies economically attractive. | High |

| Regulator-endorsed frameworks for security, audit, and data residency | Clear supervisory guidance on acceptable edge architectures would unlock sensitive workloads such as biometric authentication and real-time transaction monitoring. | Medium-High |

| Maturation of edge orchestration and observability tooling | Enterprise-scale zero-touch provisioning, policy-based orchestration, and real-time monitoring remain bottlenecks for dense edge deployments. | Medium-High |

| Demonstrated interoperability across multi-cloud and hybrid edge fabrics | Seamless workload mobility between AWS, Azure, telco edges, and on-prem nodes remains experimental in many sectors. | Medium |

Mainstream Internet of Things (IoT) technology, comprising low-power sensors, embedded compute, connectivity modules (NB-IoT, LTE-M, 5G), and cloud/edge device-management platforms, is now late-stage commercial (TRL 8-9), with large-scale deployments across manufacturing, logistics, utilities, and smart-city infrastructure. In financial services, however, end-to-end IoT stacks for regulated use cases (e.g. smart ATMs and branches, telematics-enabled asset finance, IoT-based payments) sit closer to TRL 7-8, as institutions work through integration, security, and regulatory challenges.

Key commercialisation barriers include (i) device and platform fragmentation, limiting true plug-and-play interoperability; (ii) lifecycle-management complexity for thousands of heterogeneous endpoints; (iii) persistent cyber-security concerns around endpoint hardening, key management, and supply-chain risk; (iv) uncertain liability and evidentiary status of sensor data in regulated processes; and (v) difficulty quantifying ROI once deployment and integration costs are fully accounted for. Given that core technologies are already in production, a 1-3-year horizon is realistic for scaled deployment of focused IoT solutions in banking (branch/ATM telemetry, POS health monitoring, building optimisation), while 3-7 years is a reasonable projection for pervasive, institution-wide IoT integration underpinning smart-asset finance, fully instrumented branches, and real-time risk monitoring across physical networks.

| Signpost | Comment | Likelihood |

|---|---|---|

| Commissioning of large, multi-country IoT deployments in regulated finance | Demonstrated, audited benefits (fraud reduction, downtime cuts, opex savings) across dozens of sites would sharply reduce perceived risk. | High |

| Proven business cases for banking-specific IoT (ATMs, branches, asset finance) | Robust case studies with quantified payback periods would accelerate internal investment decisions. | High |

| Declining total cost of ownership for secure, connected endpoints | Continued reductions in module, connectivity, and management costs will make dense sensorisation of branches and assets economically attractive. | High |

| Clear, durable regulatory guidance on IoT security and data use | Supervisory playbooks covering device security baselines, data residency, and evidentiary status of sensor data would unlock sensitive use cases. | High |

| Stable, scalable supply of secure IoT modules and chip-to-cloud security | Broad availability of certified secure elements and managed PKI at module level would address many cyber and supply-chain concerns. | Medium-High |

Distributed compute architectures, smart sensors, and secure device intelligence are enabling real-time risk controls, resilient operations, and next-generation customer experiences across banking channels.

Adoption of real-time edge fraud-detection will require integration, security, and operational-scaling challenges to be addressed before banks can deploy intelligence at the commercial scale of thousands of distributed payment endpoints.

| Difficulty | Barriers to Adoption |

|---|---|

| High | Many banks rely on heterogeneous, ageing terminals with limited compute capacity, requiring hardware upgrades or middleware. |

| Medium-High | Edge-deployed fraud models require frequent retraining and synchronisation with central fraud engines to avoid model drift. |

| Medium-High | Meeting auditability, explainability, and data-residency requirements across thousands of devices raises complex supervisory considerations. |

| Medium-High | Attack surfaces expand significantly when fraud analytics run on-device; secure enclaves, key rotation, and tamper-resistant hardware are required. |

| Medium-High | Continuous patching, model updates, telemetry collection, and rollback procedures must be automated to avoid operational burden. |

| Medium | Banks often operate POS/ATM fleets from multiple vendors with differing OS versions, SDKs, and security baselines, complicating deployment. |

| Medium | Retail POS sites and remote ATMs may experience unstable connectivity, requiring robust offline/near-edge fallback logic. |

| Medium | Accurate fraud detection requires alignment between real-time edge scoring and centralised behavioural models; misalignment risks false positives/negatives. |

| Medium | Upgrading terminals to support secure edge inference may require new chipsets or embedded accelerators, increasing upfront CapEx. |

| Medium | For bank-acquired POS networks, merchant IT maturity varies widely, slowing uniform deployment of edge fraud-detection capabilities. |

Surging fraud losses, rapid real-time payments growth and strong regulatory pressure create a large, urgent, and highly favourable market for real-time edge fraud-detection solutions.

Global payment and card fraud remains structurally high: the Nilson Report estimates $33.83 billion in card-fraud losses worldwide in 2023 alone, borne by issuers, merchants and acquirers. At the same time, digital and real-time payments are exploding; nearly one-fifth of all electronic payments were real-time in 2023, with the share expected to exceed one-quarter by 2028, and the real-time payments market expected to reach $198 billion by 2030.

In a conservative scenario where only 15–25% of fraud-detection spend in payments migrates to edge-optimised engines and associated orchestration by 2030, this would still imply a low- to mid-tens-of-billions dollar addressable market for real-time edge fraud-detection solutions globally, with especially strong pull in high-volume RTP ecosystems (e.g. UPI in India processing ~18 billion transactions per month) where latency and scalability requirements are most acute.

| Factor | Assessment | Overall outlook |

|---|---|---|

| Political | Governments and central banks increasingly prioritise fraud as a systemic risk; for example, UK authorities are launching new national fraud strategies and AI “super-sandboxes” with Nvidia to test authorised push-payment (APP) fraud prevention tools. | Positive |

| Economic | Persistent fraud losses and growth in both real-time payments and fraud-detection spending create strong economic incentives for solutions that reduce write-offs and chargebacks while protecting high-margin digital channels. | Positive |

| Social | Rising consumer use of instant and mobile payments, combined with public concern about scams and APP fraud, is raising expectations for proactive, real-time protection and frictionless reimbursement. | Positive |

| Technological | Rapid advances in AI, edge computing, and specialised hardware are enabling low-latency inference on terminals and gateways; dedicated forecasts for edge AI in financial services show >30% CAGR this decade. | Positive |

| Legal | Regulators are tightening liability regimes and publishing detailed payment-fraud statistics and expectations, pushing firms toward more effective real-time controls while also demanding explainability, audit trails, and robust data-protection. | Positive |

| Environmental | Although fraud-detection itself is not primarily an environmental lever, edge analytics can modestly reduce data-centre traffic and support digital-only channels that lower the physical footprint of banking. | Positive |

Banks have strong fraud, regulatory, and channel-control capabilities, but capturing the full value of real-time edge fraud detection will require bridging technical gaps in edge AI, embedded security, and large-scale device orchestration.

Most banks enter the real-time edge fraud-detection space with deep strengths in fraud operations, regulatory compliance, payments infrastructure, and customer/merchant relationships, providing a strong foundation for deploying advanced fraud controls. They also possess sophisticated data-analytics teams, enterprise security operations, and established vendor ecosystems for ATMs, POS estates, and cloud fraud systems. However, banks typically exhibit capability gaps in the technical core of this use case, and specifically edge AI model deployment, on-device ML optimisation, embedded security engineering, and device-fleet orchestration across thousands of distributed endpoints. While banks excel in the “why” (fraud losses, regulatory pressure, customer trust) and “market access” (control over payment channels, ATM/POS estates), they may lack the “how” (specialised edge ML toolchains, hardware accelerators, secure enclaves, firmware-level security, and low-latency model-serving infrastructure).

| Capability | Rationale | Current fit estimate | Current fit summary |

|---|---|---|---|

| Fraud-risk operations & analytics expertise | Understanding fraud typologies, AML/FDP workflows, risk scoring, and case management. | Strong | Banks have mature fraud teams, analytics units, and well-established central models; strong domain knowledge. |

| Regulatory & compliance expertise | Navigating payment regulations, data-residency rules, model governance, and auditor expectations. | Strong | Banks excel in compliance-heavy environments; strong capabilities in model governance and supervisory engagement. |

| Payments & channel infrastructure control | Operating ATMs, POS estates, mobile banking, card networks, and real-time payment rails. | Strong | Ownership of channels gives banks direct access to edge endpoints where fraud detection must run. |

| Vendor, merchant & acquirer partnerships | Integrating with merchant IT, payment facilitators, ATM operators, and PSP ecosystems. | Strong | Banks have deep merchant relationships and leverage acquirer networks; partnership channels already in place. |

| Cybersecurity & endpoint security | Hardening terminals, secure keystores, key rotation, zero-trust architectures. | Moderate | Strong enterprise security, but limited experience securing ML-enabled endpoints or embedded runtimes. |

| AI/ML model development for fraud | Building and validating advanced fraud models, behavioural scoring, and anomaly detection. | Moderate | Strong central-model capabilities, but limited experience with on-device inference optimisation. |

| Edge computing & embedded engineering | Deploying ML inference on POS/ATM hardware, managing compute constraints, latency, and firmware. | Moderate | Banks rarely specialise in embedded AI; rely on vendors for hardware, model runtimes, and optimisation. |

| Device management & fleet orchestration | Updating thousands of endpoints, OTA updates, telemetry, rollback mechanisms. | Moderate | Enterprise device-management exists (e.g., MDM), but specialised edge-AI fleet control is immature. |

| Data infrastructure & real-time telemetry | Handling on-device logs, local scoring outputs, and synchronising with cloud fraud engines. | Moderate | Strong central data capabilities; edge-to-core data synchronisation often requires new tooling. |

| Commercial scaling & service delivery | Rolling out fraud tools across large POS/ATM estates and delivering consistent SLAs. | Moderate | Banks can scale processes, but scaling distributed AI services across heterogeneous hardware remains challenging. |

CamIn identified and analysed 15 steps within the M&A process in terms of their ability to be optimized with AI, HPC, and IoT technologies. We isolated the 16 most promising use cases that could lead to enhanced performance, increased value to customers, and improvements in price position. We evaluated 8 Grand Challenges of unmet customer needs, where existing solutions fall short of critical success factors, revealing clear white spaces and confirmed 6 new competitive products for the client to develop based upon feasibility of technology, interest from current and new customers, and straightforward implementation within current infrastructure.