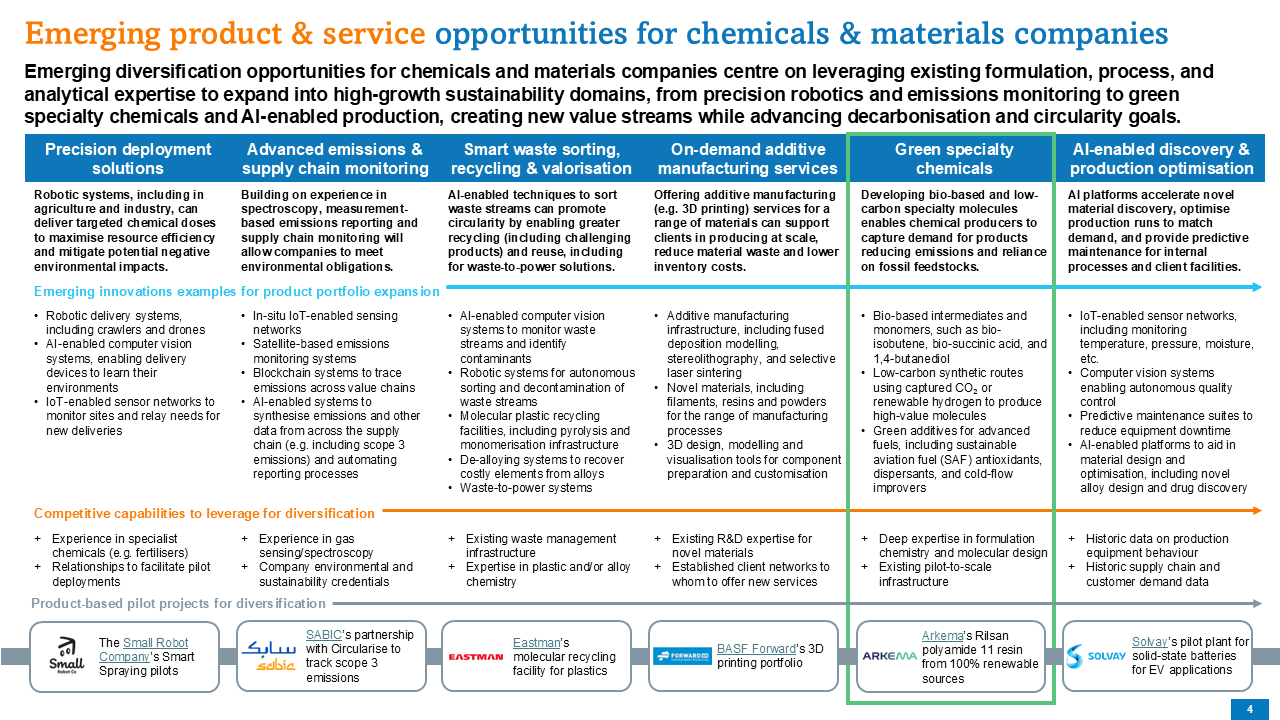

What are sustainable specialty chemicals?

Oleochemicals are chemical compounds derived from natural fats and oils, typically sourced from animal fats like tallow, or plant-based materials like palm, coconut, or soy. They are used in a wide range of applications, from personal care products and lubricants to detergents, polymers, and coatings. As bio-based alternatives to petrochemicals, sustainable specialty chemicals are central to sustainable manufacturing and circular economy strategies.

Why is diversification important for sustainable specialty chemicals manufacturers?

Diversification enables sustainable specialty chemicals manufacturers to move beyond commoditised markets and stabilise revenue streams in the face of feedstock volatility, tightening regulations, and global price pressures. By identifying adjacent high-margin products and applications, particularly those that reward bio-based sourcing and green chemistry, firms can better leverage core process capabilities like hydrogenation, esterification, ozonolysis and dimerisation to unlock new growth.

What opportunities are emerging in sustainable specialty chemicals?

New growth is emerging in sectors that prioritise biodegradability, traceability, and renewable content, such as bioplastics, sustainable lubricants, low-toxicity surfactants, and cosmetic actives. The push toward decarbonisation across industries, combined with consumer and regulatory pressure for greener supply chains, is opening premium markets for high-performance, sustainable specialty chemical derivatives.

What technologies are emerging for sustainable sustainable specialty chemicals manufacturing?

A suite of advanced technologies is reshaping sustainable specialty chemicals manufacturing, enabling producers to reduce emissions, improve process efficiency, and develop high-value bio-based products. These technologies fall into four main categories: process innovation, catalytic and biochemical conversion, digital transformation, and feedstock valorisation.

Process innovation and green chemistry

-

Continuous flow processing: Replacing traditional batch reactors with continuous flow systems improves energy efficiency, reduces solvent use, and enables tighter control over reaction conditions, particularly valuable for hydrogenation, dimerisation, and esterification reactions.

-

Reactive distillation and membrane separations: These integrated unit operations cut down on downstream processing energy and improve yield in bioderived product lines.

-

Supercritical and microwave-assisted synthesis: Emerging green process routes allow for reduced chemical inputs and shorter reaction times, supporting scalable, low-impact manufacturing.

Catalytic and biochemical conversion

-

Heterogeneous catalysis for selective hydrogenation: Novel catalysts enable greater control over reaction specificity, enhancing product quality and reducing the need for energy-intensive purification steps.

-

Enzymatic esterification and biocatalysis: Enzyme-driven processes offer milder reaction conditions and higher selectivity for producing specialty esters, lubricants, and surfactants. These processes are particularly promising for cosmetic and nutraceutical markets.

-

Microbial biosynthesis: Synthetic biology platforms are being developed to produce high-value sustainable specialty chemicals such as long-chain dicarboxylic acids and biosurfactants directly from renewable feedstocks.

Digitisation and smart manufacturing

-

Digital twins and predictive process control: Real-time simulation and optimisation of sustainable specialty chemical processes using AI and machine learning improve product consistency, reduce energy consumption, and support traceability.

-

Inline spectroscopy and smart sensors: Advanced quality monitoring tools integrated into esterification and hydrogenation lines enable faster product validation, minimising rework and waste.

Feedstock innovation and circularity

-

Valorisation of waste lipids and non-food oils: Technologies to process second-generation feedstocks like used cooking oil, tallow, or algae oil are becoming more mature, expanding the sustainable feedstock base.

-

Carbon capture and utilisation (CCU) in synthesis: Emerging processes integrate captured CO₂ into sustainable specialty chemical production chains, particularly in the synthesis of carbonate esters or enhanced fatty acid derivatives.

Excerpts from the Download

Example application area: Sustainable specialty chemicals

- Looking at key demand drivers to later analyse adoption desirability.

- Identify a long list of use cases the technologies enable and narrate what this use case is about.

Key drivers of market demand: Sustainable speciality chemicals

Sustainability is moving from a differentiator to a compliance and procurement requirement. Companies across sectors now face regulatory, financial, and reputational pressures to source low-impact, traceable, and circular-compatible specialty chemicals.

- EU Green Deal & Chemicals Strategy for Sustainability: Mandates substitution of hazardous substances and promotes sustainable chemistry innovation. Creates regulatory pull for bio-based and non-toxic alternatives across coatings, plastics, and agrochemicals.

- REACH & TSCA reform tightening: Increasing restrictions on PFAS, solvents, and VOCs drive demand for compliant, safer chemical inputs. Producers must reformulate with greener, auditable ingredients to retain market access in EU and US.

- Corporate Net-Zero and Scope 3 targets: Firms under pressure to reduce embodied emissions in supply chains. Low-carbon or renewable-feedstock chemicals become key levers for achieving decarbonisation targets.

- Extended Producer Responsibility (EPR) & Circular Economy mandates: Producers must account for recyclability and toxicity of materials throughout life. Fuels demand for green additives and binders enabling closed-loop recovery and safe reuse.

- Green procurement standards (public & private): Government tenders and corporate buyers increasingly require certified sustainable inputs. Suppliers with accredited green chemistries gain preferential access to contracts and markets.

- Consumer and brand sustainability commitments: Demand for eco-labelled and non-toxic products rising sharply in cosmetics, cleaning, and packaging. Brands push upstream suppliers toward biodegradable, bio-based, and cruelty-free formulations.

- ESG disclosure and due-diligence requirements: Mandatory sustainability reporting (CSRD, SEC, ISSB) forces firms to verify chemical sourcing. Drives adoption of traceable and third-party-certified green chemical supply chains.

- Investment and financing criteria: EU and global green taxonomies classify sustainable chemical production as eligible for green finance. Access to capital now linked to demonstrating low-carbon and non-hazardous chemical portfolios.

- Supply-chain resilience and feedstock volatility: Fossil-based inputs face price volatility and geopolitical risk. Bio-based or waste-derived feedstocks offer stable, locally sourced alternatives with lower exposure to shocks.

- Technological innovation and cost parity: Advances in biocatalysis, electrochemical synthesis, and precision fermentation lower costs. Sustainable alternatives are increasingly performance-competitive, accelerating industrial adoption.

Example technology use cases: Sustainable specialty chemicals

Bio-based, low-carbon, and recyclable formulations are replacing petrochemical incumbents across sectors, delivering equivalent or superior performance while enabling regulatory compliance, emissions reduction, and circular manufacturing.

- Additives for sustainable aviation and marine fuels: Developing multifunctional lubricity, oxidation-stability, and cold-flow improvers compatible with SAF and bio-methanol blends. Supports lifecycle CO₂ reduction and compliance with ICAO CORSIA and EU FuelEU targets.

- High-performance lubricants for electric vehicles: Formulating dielectric, low-viscosity synthetic esters and organophosphate alternatives. Improves drivetrain efficiency and cooling while reducing toxicity and metal-wear residues.

- Bio-based surfactants for home and personal care: Replacing petro-derived surfactants with plant- or microbe-derived alkyl polyglucosides and rhamnolipids. Delivers high biodegradability and lower aquatic toxicity for cosmetics, detergents, and cleaners.

- Encapsulation agents for controlled-release agrochemicals: Using biodegradable polysaccharide or protein microcapsules to replace polymer coatings. Enables precision release of nutrients or actives, reducing environmental leaching and input waste.

- Bio-based plasticisers and polymer modifiers: Replacing phthalates with citrates, isosorbide diesters, or succinate esters. Improves flexibility and thermal resistance in PVC and biopolymers with lower toxicity.

- Sustainable corrosion inhibitors for industrial systems: Formulating plant-extract-derived or amino acid-based inhibitors. Offers metal protection in cooling and hydraulic systems without persistent pollutants.

- CO₂-derived polyols for polyurethane foams and coatings: Converting captured CO₂ into reactive intermediates for polyurethanes. Reduces fossil feedstock dependence and carbon footprint in packaging, construction, and textiles.

- Biobased solvents and cleaning agents: Producing ethyl lactate, d-limonene, and glycerol derivatives as drop-in replacements for VOC solvents. Enhances worker safety and compliance with VOC and PFAS phase-out regulations.

- Catalysts and enzymes for green synthesis: Applying biocatalysis and recyclable heterogeneous catalysts to replace metal-intensive or high-temperature processes. Cuts energy demand and improves product selectivity in fine chemical manufacturing

- Recyclable and depolymerisable polymer additives: Developing dynamic covalent crosslinkers and cleavable stabilisers. Enables chemical recycling and closed-loop recovery of thermosets and composites.

Example technology use case: Additives for sustainable aviation and marine fuels

- Feasibility analysis: highlight estimated commercialisation timeline, development and adoption barriers, and any pilots, acquisitions, and start-ups.

- Desirability analysis: quantify where possible the size of the challenge it solves or size of the market it enables. Highlight the emerging opportunities and threats based on market conditions.

- Viability analysis: Identify the required capabilities necessary to develop and operate such use case and how good is the capability fit for energy and utilities companies.

Example feasibility analysis: Additives for sustainable aviation and marine fuels

Additives for sustainable aviation and marine fuels are at mid-to-high technical readiness, with several pilot-scale synthetic routes and waste-derived formulations emerging, suggesting commercial integration within 3-5 years.

Time to commercialisation

- The additive space for sustainable aviation/marine fuels is at an intermediate maturity: while conventional fuel additives (antioxidants, lubricity, corrosion inhibitors, antistatic agents) are well understood, developing novel, green, drop-in additives that enhance performance or compatibility in bio- or synthetic fuels remains under R&D and pilot scale. Some additive chemistries (e.g. bicycloalkanes, high-density cycloalkanes) have been demonstrated at lab or pilot scales to improve volumetric heating value, thermal stability, and cold-flow performance in jet fuel analogues.

- However, full qualification under aviation/marine fuel standards (e.g. ASTM D1655 / D7566 for SAF, and marine fuel additive regulations) tends to be a major barrier. Many novel additive routes are still awaiting scale-up, certification, and integration into fuel blends.

- Given the current state, a 3-5 year horizon is plausible for matured additive solutions to penetrate SAF and low-carbon marine fuels broadly. In the short term (1-3 years), additive candidates might be co-optimised with existing fuel production facilities or offered as blendstock boosters in pilot programs. In the medium term (3-5 years), successful additives could be integrated into commercial SAF/marine fuel blends, especially where feedstock variance or performance gaps (e.g. cold flow, density, stability) require tuning. In a longer horizon (5+ years), additive technologies that enable higher blending fractions or more extreme synthetic fuels (e-fuels, power-to-liquid) could see uptake, once certification and reliability are assured.

Vendors

- Universal Fuel Technologies: In a 5-month pilot, UFT demonstrated that their Flexiforming process can produce 100% synthetic SAF from renewable feedstocks using multiple pathways (methanol-to-jet, ethanol-to-jet, HEFA + ethanol) and claimed to reduce energy/hydrogen consumption vs standard ETJ routes.

- University of Illinois: A team at the University of Illinois has developed a method to convert polystyrene waste into ethylbenzene, which can serve as an additive to improve functional properties in sustainable aviation fuels.

- Topsoe: Although primarily a catalyst and technology provider for SAF production, Topsoe offers process and catalyst solutions that could enable optimised additive integration (e.g. selective upgrading, tuning of molecular product slate) in SAF production plants.

Barriers to adoption

The chemistry and functional principles of green fuel additives are mature, but adoption is currently gated by the difficulty of certification, scale-up, and feedstock economics.

| Difficulty |

Barriers to Adoption |

| High |

All new additives must undergo rigorous testing under ASTM D1655/D7566 and ISO 8217 before use in flight or shipping. Certification cycles can take years. |

| High |

Additives must remain stable and effective across multiple SAF or bio-marine fuel compositions (HEFA, ATJ, FT-SPK, etc.), complicating universal formulation. |

| Medium |

Many bio-derived additive molecules (e.g. esters, cycloalkanes) are only available at pilot scale, constraining performance testing and early deployment. |

| Medium |

Dependence on bio- or waste-derived feedstocks (lipids, lignin, or recycled aromatics) exposes producers to agricultural yield and commodity price swings. |

| Medium |

Differences in additive approval processes between FAA, EASA, IMO, and regional fuel standards slow global adoption and increase compliance costs. |

| Medium |

Limited long-duration testing in turbines or marine engines leaves uncertainty around long-term stability, corrosion, and emissions impacts. |

| Medium |

Some novel additives have hygroscopic or oxidative tendencies, requiring new blending, storage, or distribution protocols at depots and ports. |

| Medium |

Sustainable additives often have higher production costs due to bioprocessing or purification steps, limiting uptake without carbon-credit or policy incentives. |

| Medium |

Successful adoption requires co-development with SAF or marine fuel producers to ensure compatibility with refinery or hydrotreating steps. |

| Medium |

Fuel producers and additive suppliers may withhold proprietary blend data, slowing collaborative optimization and certification pathways. |

Enabling technology spotlight – PIBSI dispersants

Polyisobutylene succinimide (PIBSI) dispersants are engineered through controlled maleination and imidization chemistries to create ashless amphiphilic molecules that stabilise oxidation products and deposits in SAF.

Specific technologies deployed

-

Classical PIBSI synthesis

- PIBSIs are typically formed by (i) preparing polyisobutenyl succinic anhydride (PIBSA) from highly reactive polyisobutylene (HRPIB) and maleic anhydride (MA), followed by (ii) aminolysis/imide formation with polyamines (e.g., ethylenediamine, diethylenetriamine) to give mono- or bis-succinimides.

- The PIBSA step proceeds predominantly via a thermal Alder–ene addition of MA to the terminal olefin in HRPIB; mechanistic and kinetic work shows that both concerted ene and stepwise pathways are relevant, sensitive to PIB microstructure (vinylidene vs internal double bonds), temperature, and MA stoichiometry.

- Evidence from NMR/DFT studies and industrial kinetics work demonstrates formation of “conventional” succinic adducts as well as unconventional β-olefin maleination products at extended reaction times/temperatures, which influence adduct distribution and downstream imide quality.

- Aviation applicability and constraints: Any PIBSI considered for jet fuel service must be ashless, thermally stable, and compatible with ASTM D1655/D7566 (plus DefStan 91-091, MIL specs). Additive candidates undergo screening in JFTOT/ASTM D3241, oxidation stability (ASTM D525), conductivity, water separation, and material compatibility tests before blending approvals, which is why headgroup chemistry and purity control in PIBSI synthesis/post-treatments are critical.

-

Amidation and imidization

- Conversion of PIBSA to PIBSI proceeds via amic acid intermediates and cyclodehydration to imide, typically under solventless or high-boiling hydrocarbon conditions.

- Post-treatments (e.g. boration, glycidyl-ether functionalisation, phosphorus/boron complexation) are used to tune dispersancy, oxidative stability, and metal-surface interactions by modifying polar headgroups without sacrificing ashless character.

- Recent patent literature describes aromatic glycidyl-ether post-treatments to enhance performance and cleanliness at lower treat rates, which is important for aviation fuels where additive budgets are tight.

-

Collodial/aggregation control

- PIBSIs are amphiphiles: a solvophilic PIB tail (strongly soluble in non-polar fuel) and a polar imide/amine head.

- They adsorb on nascent oxidation products (gums, asphaltenoid/phenolic oligomers, metal-complexed particulates) via hydrogen-bonding, acid-base, and π–π/ion–dipole interactions while the PIB tail sterically stabilizes these particles in the bulk, suppressing agglomeration and surface deposition.

- Contemporary experimental/computational studies resolve how headgroup chemistry, tail length/polydispersity, and architecture (mono- vs bis-imide) control micelle-like clusters, particle zeta potential, and film formation, directly linking molecular design to deposit control and oxidation stability.

-

Bio-based routes to precursors

- Bio-isobutene (bio-IB, precursor to PIB): Metabolic and enzyme-engineered fermentative routes convert sugars (or other renewable feedstocks) to gaseous isobutene, which can be captured and cationically polymerized to bio-PIB. Global Bioenergies and others report multi-year progress and enzyme-mechanism elucidation (decarboxylase-mediated final step) toward industrialization, enabling low-CI PIB if powered by renewable energy.

- Bio-succinic acid / succinic anhydride (SAN): Fermentative succinic acid production (from glucose, glycerol, etc.) followed by dehydration to SAN is a well-mapped route; reviews detail organism engineering, membrane-assisted separations, and catalyst choices. Emerging visible-light oxidation of furanic platform molecules to SAN illustrates an alternative biomass-derived path with potentially milder conditions. Cleaner PIBSA formation: Optimising HRPIB microstructure (higher vinylidene content via improved cationic polymerization/catalyst systems) increases maleination efficiency, lowers side-products, and reduces energy demand. State-of-the-art control over HRPIB synthesis and chain transfer now allows narrow dispersity, targeted Mn (700–2,400), and higher reactivity that reduces MA and heat input for the ene step, which is favourabe for both cost and Scope 1 & 2 emissions.

Key benefits of the technology to the overall use case

PIBSIs enable cleaner, more stable, and certifiable low-aromatic SAF blends by preventing oxidation-driven deposit formation, maintaining filterability, and meeting regulatory limits.

- Oxidation and thermal-deposit control in low-aromatic SAF matrices: SAF pathways (HEFA, FT-SPK, ATJ, e-kerosene) are low in aromatics and polar heteroatom species compared to Jet A-1, which can reduce natural solvency and radical-quenching capacity. PIBSI dispersants stabilise oxidation intermediates and oligomers, interrupting auto-oxidation/radical chain growth indirectly by blocking particle-particle and particle-surface interactions, thereby extending induction times and improving JFTOT tube ratings in high-temperature tests typical for aviation. Molecular dynamics/experimental studies show synergy with phenolic/amine antioxidants, where PIBSI maintains the solubility of inhibitor-derived by-products and metal-complexed gums, further delaying filter plugging and coking in nozzles and heat exchangers.

- Cleanlieness and filerability in multi-feedstock SAF blends: Real-world SAF supply chains entail feedstock and process variability. PIBSI’s amphiphile design keeps insolubles below critical aggregation thresholds, improving filterability, cleanliness of servo valves/injectors, and depot operability across blends, particularly important when co-blending SAF with legacy Jet A-1, where trace metals and peroxide species can seed deposit formation. Historic fuel patents and deposit studies confirm PIBSI’s efficacy as ashless detergents or dispersants in hydrocarbon fuels, limiting carbonaceous deposits and sludge formation at low treat rates compatible with aviation additive budgets

- Compatibility with certification regimes and “additive budget”: A core advantage of PIBSIs is that they are ashless and can be formulated to be sulfur/metal-free, aligning with the tight elemental and thermal stability limits in ASTM D1655/D7566 and defense standards. Unlike metal-containing detergents, PIBSIs avoid ash-induced turbine deposits while offering multifunctionality (dispersancy & detergency; possible co-benefits in lubricity and conductivity packages when co-formulated), which helps stay within the limited additive treat windows permitted in aviation fuels.

- Lower life-cycle carbon and ESG differentiation: By sourcing bio-isobutene (to bio-PIB) and bio-SAN/bio-succinic acid, PIBSI manufacturers can reduce cradle-to-gate GHG intensity of the additive itself, which is important as airlines increasingly account for embedded emissions in ancillary materials. Recent reviews and TEA/LCA work indicate credible pathways to renewable carbon incorporation in both the hydrophobic (PIB) and polar (imide) fragments, particularly as bio-IB and bio-SAN scale.

Development forecast over the next 5 years

- Feedstock decarbonisation & process intensification: We expect incremental decarbonisation of PIBSI via (i) higher-vinylidene HRPIB technologies (lower energy/maleic usage), (ii) process heat integration and solvent minimisation in maleination/imidization, and (iii) pilot uptake of bio-IB (from sugar/biogenic CO₂) and bio-SAN. As economic signals (e.g., SAF mandates, carbon pricing) strengthen, suppliers with documented LCA for PIBSI (including energy sourcing) will differentiate. Publications and patents on post-treatment chemistries (e.g., glycidyl-ether functionalisation) will continue to target lower treat rates and broader fuel-matrix robustness (HEFA, FT-SPK, ATJ).

- Formulation science for SAF variability and co-additive synergies: We expect designed co-packages pairing PIBSI with hindered phenolics/arylamines (antioxidants), metal deactivators, and conductivity improvers, validated on ASTM D7566 annex fuels. Molecular simulation and machine-learning-guided formulation will be used to balance oxidation control, cleanliness, filterability, and water separation under tight additive budgets. Peer-reviewed studies already demonstrate antioxidant–dispersant synergies and nanoparticle aggregation suppression; translating this into qualification-ready packages is the logical next step.

- Technical certification and standard-setting integration: As more SAF pathways reach commercial scale, additive packages (including PIBSI-containing blends) will be proposed/tested under ASTM D7566 and aligned with D1655 “co-processed” routes. The FAA/IATA certification guidance indicates pathways for demonstrating compatibility via JFTOT (D3241), oxidation stability (D525), materials compatibility, and system tests; we should see PIBSI-based packages moving through OEM and third-party rigs to support broader blending limits and operational robustness claims in warm/cold extremes. Successful packages will be documented in industry circulars and annexes, enabling airline adoption at scale.

- Further advancements in green and bio-based chemistries: Beyond bio-IB/bio-SAN, R&D is trending toward: electro/photochemical oxidation of furans to SAN, continuous-flow maleination with better heat/mass transfer and reduced side-products, and catalyst-enabled low-temperature ene processes to cut energy input. If demonstrated at pilot scale with robust QA/QC, these could materially lower additive CI and cost, while tightening product distributions (beneficial for aviation approvals).

- Building the evidence base in turbines and marine engines: While PIBSI efficacy is well-established in lubricants and ground fuels, expect more public data from turbine-relevant rigs and marine medium-speed engine tests using low-aromatic/renewable fuels, to de-risk long-duration stability/corrosion questions. As those data sets mature, adoption barriers tied to uncertainty of long-term impacts should diminish.

Example desirability analysis: Additives for sustainable aviation and marine fuels

Size of opportunity

The global aviation fuel additives market (which today largely serves conventional jet fuels) is projected to grow from around $870 million in 2024 to about $1.3 billion by 2031, representing a ~6.2 % CAGR. Meanwhile, the broader sustainable aviation fuel (SAF) sector is expected to scale rapidly: one forecast puts the global SAF market at $1.6 billion in 2024 and growing to $25.6 billion by 2030.

Because additives are a value-added component of fuel blends, if green additive solutions capture even a modest premium or share in the evolving SAF/low-carbon fuel space, the total addressable market (TAM) could represent tens to potentially hundreds of millions of dollars annually in recurring revenues.

Moreover, mandates and blending obligations (e.g. SAF blending rules in the EU) create a compulsory growth tailwind for fuel volumes, indirectly expanding the demand base for additive solutions.

In short, as SAF and low-carbon marine fuels scale, there is a built-in “adjacent market” for performance and compatibility additives, making this a high-leverage niche.

External threats and opportunities

| Factor |

Assessment |

Overall outlook |

| Political |

The EU’s proposed SAF blending mandates and emissions regulations in many jurisdictions, generate compulsory demand. However, political shifts or mandate delays may slow downstream adoption. |

Positive |

| Economic |

Fuel cost pressures and carbon pricing may help green additives justify premiums, while economies of scale in SAF production will reduce cost gaps. High initial R&D and scale-up costs may impede smaller entrants. |

Positive |

| Social |

Airlines, shipping firms, and downstream users face reputational and investor pressure to decarbonize, which supports uptake of performance-enhancing, low-carbon additives. |

Positive |

| Technological |

Advances in catalysis, biomass- or waste-derived feedstocks, and integration with SAF production pathways improve feasibility. Ensuring additive stability and long-term performance is nontrivial. |

Positive |

| Legal |

Stringent certification and additive approval requirements (ASTM, ISO, etc.) pose a legal barrier; but once cleared, such regulation also becomes a moat. |

Negative |

| Environmental |

Additives that reduce emissions, improve fuel efficiency, or enable higher blend rates will have strong positive environmental rationale. However, lifecycle carbon and feedstock sourcing must be credible and auditable. |

Positive |

Example viability analysis: Additives for sustainable aviation and marine fuels

Specialty chemicals firms have strong core capabilities in formulation, process scale-up, and compliance, but need sector-specific partnerships and certification access to move from additive R&D to large-scale adoption.

Capability fit assessment

A typical specialty chemicals firm is well-positioned to enter the sustainable aviation and marine fuel additive market, with strong chemistry, formulation, and regulatory expertise, but may need to expand into new feedstock sourcing, certification processes, and aerospace/marine partnerships to capture the opportunity. Overall, these firms possess the “how” (molecular design, production, and QA) but must strengthen the “where” (aviation/marine value-chain access) to achieve viability.

| Capability |

Rationale |

Current fit estimate |

Current fit summary |

| Catalysis and formulation chemistry |

Core strength in designing multifunctional molecules (lubricity improvers, antioxidants, cold-flow modifiers). |

Strong |

Most specialty firms already develop additives for fuels and lubricants with scalable synthetic know-how. |

| Process engineering and pilot-scale synthesis |

Scaling novel chemistries from lab to production at consistent purity. |

Strong |

Extensive pilot-to-commercial synthesis infrastructure, including batch and continuous processing for fine chemicals. |

| Regulatory and certification expertise |

Navigating REACH, TSCA, IMO, and ASTM fuel additive certification standards. |

Strong |

Large chemical producers maintain in-house regulatory teams and third-party testing partnerships for fuel approval pathways. |

| Feedstock and supply-chain integration |

Securing sustainable bio-based or CO₂-derived intermediates. |

Moderate |

Firms may rely on external biorefineries or carbon-utilisation startups for novel precursors. |

| Aviation and marine industry partnerships |

Collaborating with OEMs, refineries, and airlines/shipping operators for performance validation. |

Moderate |

Limited direct relationships outside petrochemical incumbents; growing through initiatives like Clean Skies for Tomorrow. |

| Lifecycle assessment (LCA) and ESG reporting |

Demonstrating verified GHG and toxicity reductions for green-chemistry claims. |

Moderate |

Many firms have strong sustainability teams, but fuel-specific LCA standards (CORSIA, FuelEU Maritime) require tailored frameworks. |

| Digital process optimisation and analytics |

Using data-driven process control to optimise yields and emissions. |

Moderate |

Advanced analytics in production exist, but may need adaptation for bio-feedstock variability and additive precision blending. |

| Bio-based and CO₂-based synthesis expertise |

Developing renewable intermediates from fermentation, gas fermentation, or CO₂ conversion. |

Moderate |

Growing R&D presence (e.g. collaborations with LanzaTech, Twelve), though limited large-scale deployment. |

| Commercial scaling and route-to-market |

Marketing new additives to energy and transport sectors. |

Moderate |

Strong B2B distribution networks, but entry into aviation/marine fuel ecosystems requires alignment with refinery and OEM partners. |

| Testing and certification infrastructure (ASTM/IMO/ICAO) |

Conducting full compatibility and emissions testing under aviation/marine operating conditions. |

Weak |

Certification facilities are often external; requires partnerships with test houses or OEMs to validate additive safety and performance. |

Example Decision Matrix

CamIn conducted 13 interviews with senior management and assessed 20 key application areas to evaluate the client's capabilities and potential opportunities. We reviewed 200 key molecular families and confirmed the 10 highest priority strategic product options, including assessing potential geographic markets.

.svg)