Case Study

IoT and edge roadmap for banking services

Identifying high-value IoT and edge services to drive banking growth

Identifying high-value IoT and edge services to drive banking growth

CamIn works with early adopters to identify new opportunities enabled by emerging technology.

of CamIn’s project team comprised of leading industry and technology experts

A leading banking client sought to identify, validate, and prioritise IoT and edge-enabled services to unlock new revenue streams and guide a five-year, $50 million innovation investment with a clear, de-risked roadmap

AI, digitalisation, and automation

The client was performing strongly but faced increasing pressure to act on IoT and edge computing opportunities within a fragmented and hype-driven landscape.

They aimed to identify credible, high-value service opportunities and define a structured innovation roadmap aligned to strategic priorities.

The objective was to unlock new multi-million-dollar revenue streams, reduce time-to-market risks, and de-risk a $50 million innovation portfolio through evidence-based prioritisation.

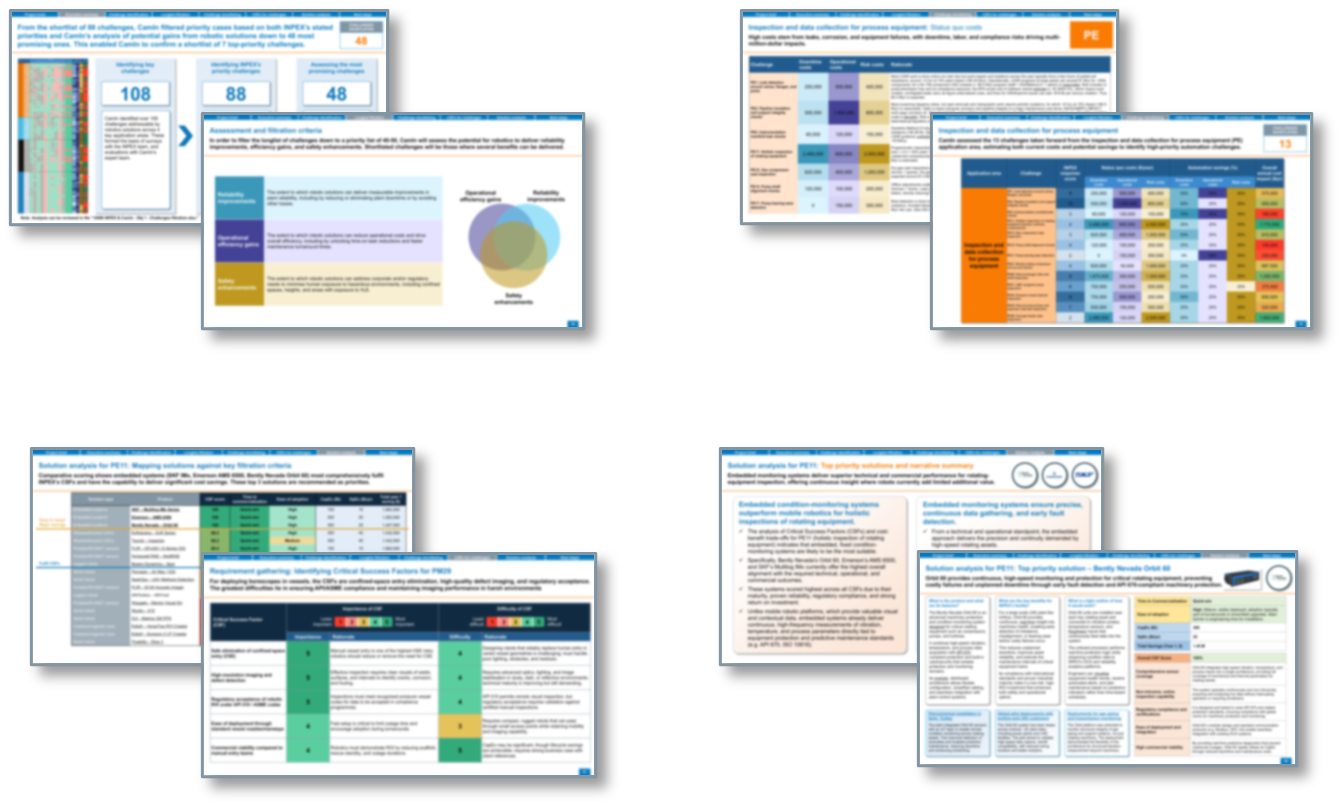

110 | Mapped IoT and edge use cases across customer experience, fraud prevention, branch operations, and trading infrastructure to establish a comprehensive opportunity landscape. |

24 | Assessed relevant technologies for maturity, scalability, and alignment with financial services requirements to ensure focus on commercially viable innovation areas. |

18 | Prioritised high-value use cases based on feasibility, desirability, and strategic fit to narrow the opportunity set to actionable initiatives. |

10 | Validated product and service concepts and structured them into a five-year roadmap with defined implementation phases and investment priorities. |

CamIn identified 110 opportunities and confirmed 10 high-value products for investment, forming a clear five-year roadmap.

The client is aligning internal stakeholders and progressing towards pilot business cases and investment approvals.

The work de-risked a $50 million innovation portfolio and enabled targeted multi-million-dollar revenue opportunities.

Download our detailed case study to learn more about how CamIn and our hand-selected expert project team delivered these results for our client.

.svg)

IoT and edge computing in financial services refer to connected devices, sensors, and local data processing systems that enable real-time data capture and decision-making at or near the point of transaction. Rather than relying solely on centralised cloud systems, banks can process data locally to reduce latency, improve resilience, and enable immediate actions across customer interactions, operations, and risk management.

Financial institutions are under pressure to deliver faster, more secure, and more personalised services while managing rising operational complexity and regulatory scrutiny. Large volumes of data are generated across branches, ATMs, payment terminals, and trading systems, yet much of this data remains underutilised due to processing constraints.

Edge computing allows institutions to act on this data in milliseconds, enabling real-time fraud detection, faster authentication, and improved customer experience. It also supports cost reduction by optimising physical infrastructure and reducing reliance on central processing. Strategically, it enables new service models such as embedded finance and intelligent payments, strengthening competitiveness and unlocking new revenue streams.

IoT and edge computing are moving beyond experimentation towards targeted deployment in high-value areas. The most relevant opportunities are those that combine immediate operational improvements with scalable service innovation, particularly where latency, security, and data ownership are critical.

Banks are beginning to leverage edge-enabled devices to deliver more contextual and responsive customer interactions. In the short term, quick wins include intelligent ATMs and branch devices that adapt interfaces based on customer profiles and behaviour, improving conversion rates and reducing service time.

Mid-term opportunities focus on integrating edge analytics into mobile and payment devices, enabling real-time personalisation of offers at the point of interaction. This can increase cross-sell effectiveness and customer lifetime value without relying on centralised data processing delays.

Long-term potential lies in hyper-personalised financial ecosystems, where connected devices continuously feed behavioural data into edge systems to anticipate customer needs. This could reshape how financial products are delivered, shifting from reactive to predictive engagement models. However, execution depends on trust, data governance, and seamless integration across channels.

Fraud prevention is one of the most commercially impactful applications of edge computing. Immediate opportunities include deploying edge-based authentication at payment terminals, enabling biometric verification and anomaly detection without latency.

In the mid-term, institutions can embed machine learning models directly into devices, allowing transactions to be assessed locally in real time. This reduces fraud losses while improving approval rates and customer experience. It also reduces dependency on central fraud systems, improving resilience.

Long-term, edge-enabled distributed security architectures could enable decentralised fraud detection networks, where insights are shared across devices without exposing sensitive data. This could significantly reduce systemic risk, though it introduces new challenges in standardisation and regulatory alignment.

Physical infrastructure remains a major cost centre for banks, and edge technologies provide a pathway to optimise these assets. Short-term gains include predictive maintenance for ATMs and branch equipment, reducing downtime and service disruptions.

Mid-term opportunities involve intelligent asset management, where connected devices monitor usage patterns and dynamically allocate resources across locations. This can reduce operational expenditure and improve service availability.

Long-term transformation could see branches evolve into fully digitised, autonomous service hubs with minimal staffing requirements. While this reduces cost, it requires careful balancing with customer trust and regulatory expectations around service accessibility.

Latency is a critical factor in trading and treasury functions, making edge computing highly relevant. Immediate opportunities include deploying local processing for market data analysis, improving execution speed and decision accuracy.

In the mid-term, edge-enabled infrastructure can support distributed trading systems that reduce reliance on centralised data centres. This improves resilience and reduces the risk of single points of failure.

Long-term, the integration of edge computing with advanced analytics could enable fully automated trading environments operating at microsecond speeds. While offering competitive advantage, this also introduces governance challenges and potential systemic risks that must be actively managed.

The enabling technology landscape for edge computing in financial services is evolving rapidly, with a mix of hardware, software, and security innovations shaping deployment strategies. The most relevant developments are those that balance performance, scalability, and regulatory compliance.

Edge AI enables machine learning models to run directly on devices such as payment terminals and ATMs. Its primary strength is the ability to deliver real-time insights without relying on cloud connectivity, which is critical for fraud detection and customer interactions.

However, limitations remain around model complexity and update cycles, as deploying and maintaining models across distributed devices can be operationally challenging. Opportunities lie in improving model compression and federated learning techniques, which allow models to learn from distributed data without central aggregation.

The main threat is the risk of inconsistent model performance across devices, which can impact decision quality and regulatory compliance if not managed effectively.

Sensors and connected devices form the foundation of edge-enabled services, capturing data across physical and digital touchpoints. Their strength lies in enabling visibility into previously opaque processes, such as customer behaviour in branches or asset performance.

Weaknesses include security vulnerabilities and integration challenges with legacy systems. Many financial institutions underestimate the complexity of managing large device networks at scale.

Opportunities exist in expanding sensor deployment to support new services such as usage-based financing or ESG monitoring. However, increasing device proliferation also expands the attack surface, requiring robust device-level security strategies.

Edge infrastructure includes the hardware and software platforms that enable local data processing. These systems are critical for reducing latency and supporting real-time applications.

Their strength is scalability, as they can be deployed incrementally across locations. However, they introduce operational complexity, particularly in managing distributed environments and ensuring consistent performance.

Opportunities lie in hybrid architectures that combine edge and cloud capabilities, allowing institutions to balance speed and scale. The key threat is underinvestment in orchestration capabilities, which can lead to fragmented systems and reduced ROI.

Security is a defining factor in the adoption of edge computing in financial services. Emerging solutions include device-level encryption, secure enclaves, and distributed identity management systems.

These technologies enable secure data processing at the edge, reducing exposure to centralised breaches. Their strength lies in enhancing resilience and compliance with data protection regulations.

However, they can be costly to implement and require specialised expertise. Opportunities exist in leveraging these architectures to enable new services that rely on secure, real-time data processing.

The primary threat is regulatory misalignment, as evolving data privacy requirements may outpace technological implementation, creating compliance risks if not proactively addressed.